Exceptional and unforgettable Moments of Truth fuel customer delight and loyalty. So too do pointless and broken interactions douse brand devotion. Unfortunately, disappointment carries more weight. Research undertaken by Richard Normann several decades ago revealed that it takes twelve positive Moments of Truth to recover from one failure.

Knowing this, it makes sense to prioritize efforts on removing the pointless and fixing the broken moments first for the greatest return. A practical approach to doing this is to first determine what customers need and want from their banking relationship and second to identify and refine common events where the bank is failing to deliver against those needs.

Starting with Customer Priorities

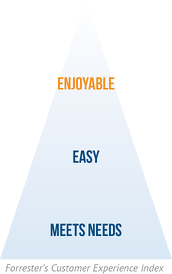

Forrester, PeopleMetrics, and others have identified three universal customer experience priorities. These are:

Meeting customer needs. Customers say their bank meets their needs when they can achieve their personal and financial goals through the products, services and support offered by their chosen financial institution.

Being easy to bank with. Deliver enjoyable experiences across all touch points – opening an account, depositing funds, applying for a loan, meeting with an advisor. The bank makes it simple, clear and easy.

Making an emotional connection. The bank’s processes and staff behave in a way that make the customer feel appreciated, cared for, and valued by that institution.

Where Banks Often Fail

Through our banking industry research we have found three common Moments of Truth where customers’ wants and needs are not being met – moments that can fracture the relationship.

1. The Denial of a Loan Application and Not Meeting Customer Needs

Making This Customer Experience Real

Mr. Peterson’s construction business is booming. He has more customers than he can serve and is ready to bring some additional guys onto the team. But to make this happen, he needs another truck. He stops into his local bank branch to fill out the necessary loan paperwork. With a long, 15-year relationship and an account in good standing, he figures this is going to be a breeze. He’s already put a deposit down at the dealership. After a 30-day wait and a ton of paperwork, he receives a letter informing him that his loan application has been denied.

Why This Matters to Your Banking Customers

On a rational level the bank failed to help Mr. Peterson capitalize on the opportunity to grow his business. The bank hasn’t met his needs.

On an emotional level he feels rejected, perhaps a little embarrassed, likely betrayed. For years he has trusted this institution with his hard-earned money and now discovers that level of trust is not reciprocated.

Meet Needs by Redesigning the Loan Denial Process

Consider redesigning the loan denial process to include:

- Suggested steps the customer can take to improve their credit score.

- Offering assistance with budgeting and saving.

- Making them aware of any personal and/or business financial management tools you offer.

- Presenting some practical alternatives for them to consider to achieve their goals.

- Making the experience more personal by sharing the news – and recommended options for the future – in person or over the phone.

- Scheduling a future appointment to check in on progress and look at options that may be available at a later time.

2. Mobile Banking Doesn’t Do What It Promises and Isn’t Easy to Bank With

Making This Customer Experience Real

Brian has a new job that means he travels cross-country four nights out of five. His Smartphone is his lifeline. He uses it to check in for flights, source speedy cab rides in unfamiliar cities, purchase his morning coffee, and deposit his ever-growing expense checks into his regional bank’s checking account back home. That is until one day he receives an error message informing him that the dollar value of the check he is attempting to deposit exceeds the bank-approved limits. He must visit a branch or mail in the check to deposit the funds.

Why This Matters to Your Banking Customers

The bank has made something that promises to be easy difficult. Because the customer expects a lot from his mobile experiences the failure to meet those expectations can be more detrimental than if he hadn’t had the opportunity to engage via that channel in the first place. The customer ends up feeling annoyed and frustrated and without the funds perhaps even worried about overdrawing his account.

Prevent Mobile Disappointment to Keep It Easy

- Avoid surprises. Explain regulations, limitations, and benefits upfront in simple, clear, jargon-free language. Customers are typically reasonable if they feel there is a clear rationale for the rules they are required to follow. Tell them in plain English and help them avoid being disappointed.

- Listen and learn from your customers. There may be some aspects of your mobile solution that were not well thought out or designed from a user-perspective. It’s not too late to listen to your users, learn what they need, uncover their frustrations and make some simple fixes. Capturing and acting on customer feedback at key moments of truth is an essential ingredient in your customer experience approach.

3. Selling the Customer’s Mortgage and Undoing an Emotional Connection

Making This Customer Experience Real

Joe and Amy love their bank. After five years of scrimping and saving and living in Joe’s parents’ basement they have finally bought their first home. They feel as if they are parting from a dear friend as they shake the hand of their mortgage advisor the day of closing. The boxes are empty, the pictures are hung on the walls, their new life is settling into a happy routine when a letter arrives on letterhead from an unknown financial institution. The document tells them that their bank has sold their mortgage to this organization.

Why This Matters For Your Banking Customers

Unlike in the case of a loan denial, these customers love their bank – it helped to make their dream come true. But now they feel inconvenienced. The automatic payments they had set up for their monthly mortgage payment need to be re-established. But, more importantly, on an emotional level they feel irrelevant. A relationship that felt so significant to them seems to have no value to their bank. In an instant they turn from feeling secure in the promise of a long partnership to seeing their bank as a place to transact. And now there is another bank they can transact with too – perhaps they’ll offer better HELOC rates when the time comes, better financial products for their future needs. The bank has turned a monogamous relationship into one that is now polygamous – giving the customer permission to seek support elsewhere.

Face the Possibility of a Mortgage Sale Head-On

- Explain to the customer the likelihood of the mortgage being sold and what that means to them and their relationship with the bank.

- Contact the customer to see if they have questions about the sale of their loan.

- Check in at key points to offer advice, guidance, and support aligned with customer lifecycle needs.

These are just three of many moments of truth that we see creating frustration or disappointment for banking customers. The lesson here is that by starting to deliberately eliminate or redesign the broken moments you will secure the loyalty and advocacy of more of your customers more of the time.

Have you had to face a customer that had one of these 3 moments happen to them? How did you handle it?

–Kate Feather

If you’d like to learn more about banking customer experience, then sign up for our email-based elearning course. Just click on the button below, enroll, and we'll send helpful articles and useful resources right to your inbox. And best of all, it's free!

%20(1).png)